The Harvest Price Problem for California Tree Nut Growers

The structure of California tree nut markets creates a fundamental financial tension for growers: harvest occurs over a 6–10 week window in late summer and fall, during which enormous volumes of almonds, pistachios, and walnuts enter the market simultaneously. This concentrated supply peak predictably depresses spot prices at exactly the moment growers need cash to pay harvest labor, equipment, and operating loan obligations.

Growers who are forced to sell immediately at harvest to meet cash obligations are systematically disadvantaged compared to handlers and processors who can hold inventory and sell into stronger market windows in the months that follow. Inventory-backed financing closes this gap — it allows growers to access the liquidity they need to operate without liquidating inventory at harvest-low prices.

How Warehouse Receipt Financing Works

Warehouse receipt financing (also called field warehouse financing or commodity-backed lending) uses stored inventory as collateral for a short-term credit facility. The process works as follows:

Step 1: Delivery to a licensed public warehouse. The grower delivers certified-weight, certified-grade product to a licensed public cold storage warehouse. The warehouse issues a negotiable warehouse receipt documenting: the identity of the depositor, the commodity description, the weight and grade, and the storage location.

Step 2: Pledge of warehouse receipt to lender. The grower endorses the warehouse receipt to a lender — typically their agricultural lender, Farm Credit, or a commodity finance specialist. The lender holds the receipt as collateral security for the loan.

Step 3: Credit advance against commodity value. The lender advances a percentage of the commodity’s current market value — commonly 70–80% of the CME or Almond Board benchmark price — as a short-term operating loan. Interest rates for warehouse receipt financing are typically lower than unsecured operating credit because the lender holds tangible, liquid collateral.

Step 4: Release of inventory and loan repayment. When the grower sells the inventory at a price and time of their choosing, the proceeds retire the loan (principal plus interest), and the warehouse receipt is released to the buyer’s warehouse account.

California Agricultural Lenders and Commodity Financing Programs

Farm Credit West, Rabobank (now a division of Compeer Financial), Wells Fargo Agricultural Finance, and Bank of the West all offer commodity-backed lending programs specifically structured for California tree nut producers. Agricultural credit unions throughout the San Joaquin Valley provide similar programs for members.

The Almond Board of California and the American Pistachio Growers organization both publish resources on commodity financing options for members. For growers unfamiliar with warehouse receipt financing, these organizations are good starting points for understanding the process and identifying appropriate lenders.

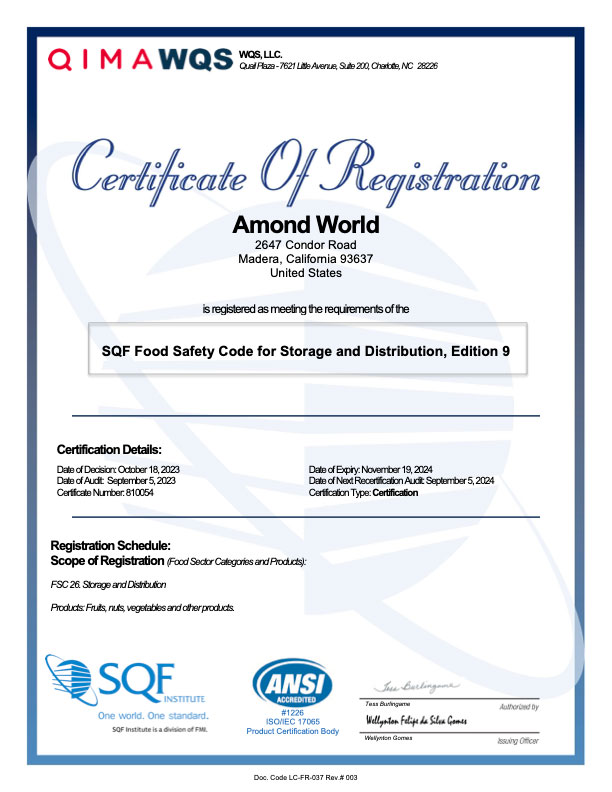

Requirements for Cold Storage Warehouse Receipt Financing

Not all cold storage facilities can issue negotiable warehouse receipts. To issue receipts usable for financing, the facility must be licensed as a public warehouse under California or federal warehouse regulations. For federally licensed warehouses, USDA Warehouse Act licensing provides the legal framework that lenders rely on. Verify warehouse licensing status before selecting a storage facility if you intend to use inventory financing.